- Beranda

- Komunitas

- News

- Berita Luar Negeri

U.S. Is No. 1, China Is So Yesterday.............kacian deh loh :D:D

TS

AkuCintaNanae

U.S. Is No. 1, China Is So Yesterday.............kacian deh loh :D:D

Quote:

U.S. Is No. 1, China Is So Yesterday

A decade ago, the fabled Goldman Sachs report “Dreaming With BRICs” predicted that China’s gross domestic product would overtake the U.S.'s sometime in the 2020s. The World Bank study released last month was the hype to end all hype. It advanced the date of doom to the end of this year.

Last time I looked (yesterday), the U.S. economy in 2013 was three times larger than the Chinese (in real 2005 dollars, according to the magnificent historical data set of the U.S. Department of Agriculture’s Economic Research Service). Did the Chinese economy triple in the last four months?

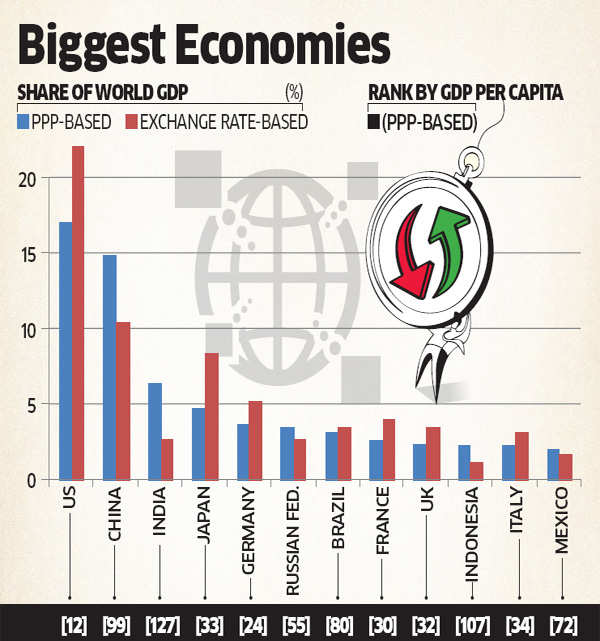

Well, no, the World Bank would retort. Then it would invoke the magic three P’s: purchasing-power parity, which it has just recalculated to arrive at the end of U.S. economic hegemony. This yardstick takes into account that a dollar buys a lot more in Beijing than in Bethesda, Maryland. According to the Big Mac index, for instance, the McDonald's hamburger costs 40 percent more stateside than in the Middle Kingdom.

I would go one better by throwing in my very own barber index. A haircut in Palo Alto, California, sets you back $25; the average in Shanghai is 5 bucks. So add 40 percent to China’s dollar GDP. Or even multiply by it by 5?

Nice game, but it doesn’t reflect real economic power. When China imports technology from the U.S. or high-tech weaponry from Israel, it has to pay in dollars. Ditto when it gobbles up African mines or buys the loyalty of developing countries with foreign aid. Tuition for Chinese students at Stanford University is also billed in dollars. Same with Beemers and Porsches.

In other words, PPP is a handy way to inflate a developing country’s economy. But it is a rubbery standard when measuring the real clout of nations -- especially when U.S. per capita GDP (in dollars) is eight times bigger than China’s, which is just a shade higher than Peru’s.

If “America, the Has-Been” were a TV series, it would now be in its fifth season. The first, Decline 1.0, opened in the 1950s, after the Soviets launched their Sputnik. Weren’t they growing and arming faster? The myth of the “missile gap” gripped the land. Yet a generation later, the Soviet Union was no more, dying peacefully on Christmas Day 1991 and leaving behind 15 orphan republics.

Decline 2.0 swept the nation during the Vietnam War, and once more the U.S.'s best days were over, intoned a chorus of pundits and politicos. But it remained far and away No. 1 economically and strategically, making up for the loss of South Vietnam by eventually corralling Hanoi as a quasi-ally against China.

Decline 3.0 was initiated in 1979 by President Jimmy Carter when he moaned in his so-called malaise speech that the U.S. was beset by “a crisis of confidence,” one “that strikes at the very heart and soul and spirit of our nation.” The depression ended with Ronald Reagan who proceeded to out-arm the Soviet Union. By 1984, it was “morning again in America.”

Decline 4.0 cast Japan as the next No. 1. Having failed in Pearl Harbor with their bombers, these super-samurais would now triumph with their Toyotas and Sonys. Like China, Japan had been growing at double-digit speed, but after 1988 it was downhill, and it isn't the end yet. Four years later, the U.S.'s longest expansion began. It lasted essentially until the recession of 2007-10.

Now it is Decline 5.0, starring China as the master of the universe. The World Bank should have looked at history. As early as 1984, China’s growth peaked at 15 percent. Now, the rate is down to one-half that. The sluggish world economy plays a part, but the underlying reasons are structural.

Spectacular growth is always easy when countries start at zero, as did Taiwan and South Korea. Or as did destroyed economies such as Japan’s and West Germany’s. Essentially, they all followed the same growth model: overinvestment, underconsumption, “exports first” and an artificially cheapened currency. West Germany once hit 8 percent, and the Little Dragons boasted rates as impressive as China’s in its heyday. In this decade, Taiwan is down to an average of 3.75 percent, South Korea to 3, and Japan to 1.

The law of diminishing returns always takes its toll, with ever more capital inputs generating ever smaller additions to output. Also, the Little Dragons soon ran out of cheap labor as their countrysides emptied out.

True, runs a classic riposte, but China is different because it still has an “industrial reserve army” of 700 million eager to flood into the cities. Ample low-wage labor will continue to fuel rapid growth, so China won't turn into tomorrow’s Japan.

Look again. China’s demography is a disaster. About 2015, the seemingly boundless labor pool will begin to shrink. One reason is rapid aging, which presages that China will become old before it becomes rich. By 2050, China will have lost one-third of its working-age population. Meanwhile, the U.S. will bestride the earth as the youngest industrialized nation after India.

Also in this decade, the number of China’s dependents will start to soar. The U.S. curve will rise only slowly, due to high fertility and immigration, two classic sources of rejuvenation. By midcentury, one Chinese worker will have to support two dependents, a ratio worse than anywhere in the West. If ample labor is the food of growth, China is looking at starvation.

Another data set should also have given pause to the World Bank: China’s cost advantage in manufacturing is almost history. Wages have risen exponentially since 2000, by an average of 19 percent annually. The figure for the U.S. was 4 percent.

As a study by Boston Consulting notes, “By around 2015, the total labor-cost savings of manufacturing many goods in China will be only 10 to 15 percent annually when actual labor content is factored in.” Subtract from this margin the cost of shipping and a global supply chain. So jobs are already wandering off to cheaper locales. Today it is Vietnam; tomorrow it will be Africa. Or the jobs will come home to the U.S., nourishing the country’s “re-industrialization” in tandem with plentiful cheap energy from fracking.

Finally, China’s politics are wrong. Authoritarian modernization -- call it “modernitarianism” -- runs up against its built-in limits, as did the Soviet Union’s. Frenzied industrialization under the knout of the party is easy, but the knowledge economy takes its cues from the markets. The watchword is “freedom” -- for entrepreneurs and capital, ideas and innovation. There is no Silicon Valley in China’s future.

Look at the assets that multiply returns. For instance, ask where human capital is being generated. U.S. education is always said to be in crisis. But 17 of the world’s top 20 universities are in the U.S., and 34 of the top 50. No other country produces more doctorates in science and engineering. Although 40 percent of the recipients come from abroad, two-thirds of them stay. Add triadic patents and citations in scientific journals, and it isn’t even a race between China and the U.S. This serendipitous story will continue, but it comes with a warning: The U.S. has to remain open and welcoming.

For now, don't waste time staring at the PPP snapshots, as kneaded and pummeled by the World Bank. They reflect the price of Big Macs, not III: innovation, ingenuity and invention. It will take a long time before China catches up -- if ever.

A decade ago, the fabled Goldman Sachs report “Dreaming With BRICs” predicted that China’s gross domestic product would overtake the U.S.'s sometime in the 2020s. The World Bank study released last month was the hype to end all hype. It advanced the date of doom to the end of this year.

Last time I looked (yesterday), the U.S. economy in 2013 was three times larger than the Chinese (in real 2005 dollars, according to the magnificent historical data set of the U.S. Department of Agriculture’s Economic Research Service). Did the Chinese economy triple in the last four months?

Well, no, the World Bank would retort. Then it would invoke the magic three P’s: purchasing-power parity, which it has just recalculated to arrive at the end of U.S. economic hegemony. This yardstick takes into account that a dollar buys a lot more in Beijing than in Bethesda, Maryland. According to the Big Mac index, for instance, the McDonald's hamburger costs 40 percent more stateside than in the Middle Kingdom.

I would go one better by throwing in my very own barber index. A haircut in Palo Alto, California, sets you back $25; the average in Shanghai is 5 bucks. So add 40 percent to China’s dollar GDP. Or even multiply by it by 5?

Nice game, but it doesn’t reflect real economic power. When China imports technology from the U.S. or high-tech weaponry from Israel, it has to pay in dollars. Ditto when it gobbles up African mines or buys the loyalty of developing countries with foreign aid. Tuition for Chinese students at Stanford University is also billed in dollars. Same with Beemers and Porsches.

In other words, PPP is a handy way to inflate a developing country’s economy. But it is a rubbery standard when measuring the real clout of nations -- especially when U.S. per capita GDP (in dollars) is eight times bigger than China’s, which is just a shade higher than Peru’s.

If “America, the Has-Been” were a TV series, it would now be in its fifth season. The first, Decline 1.0, opened in the 1950s, after the Soviets launched their Sputnik. Weren’t they growing and arming faster? The myth of the “missile gap” gripped the land. Yet a generation later, the Soviet Union was no more, dying peacefully on Christmas Day 1991 and leaving behind 15 orphan republics.

Decline 2.0 swept the nation during the Vietnam War, and once more the U.S.'s best days were over, intoned a chorus of pundits and politicos. But it remained far and away No. 1 economically and strategically, making up for the loss of South Vietnam by eventually corralling Hanoi as a quasi-ally against China.

Decline 3.0 was initiated in 1979 by President Jimmy Carter when he moaned in his so-called malaise speech that the U.S. was beset by “a crisis of confidence,” one “that strikes at the very heart and soul and spirit of our nation.” The depression ended with Ronald Reagan who proceeded to out-arm the Soviet Union. By 1984, it was “morning again in America.”

Decline 4.0 cast Japan as the next No. 1. Having failed in Pearl Harbor with their bombers, these super-samurais would now triumph with their Toyotas and Sonys. Like China, Japan had been growing at double-digit speed, but after 1988 it was downhill, and it isn't the end yet. Four years later, the U.S.'s longest expansion began. It lasted essentially until the recession of 2007-10.

Now it is Decline 5.0, starring China as the master of the universe. The World Bank should have looked at history. As early as 1984, China’s growth peaked at 15 percent. Now, the rate is down to one-half that. The sluggish world economy plays a part, but the underlying reasons are structural.

Spectacular growth is always easy when countries start at zero, as did Taiwan and South Korea. Or as did destroyed economies such as Japan’s and West Germany’s. Essentially, they all followed the same growth model: overinvestment, underconsumption, “exports first” and an artificially cheapened currency. West Germany once hit 8 percent, and the Little Dragons boasted rates as impressive as China’s in its heyday. In this decade, Taiwan is down to an average of 3.75 percent, South Korea to 3, and Japan to 1.

The law of diminishing returns always takes its toll, with ever more capital inputs generating ever smaller additions to output. Also, the Little Dragons soon ran out of cheap labor as their countrysides emptied out.

True, runs a classic riposte, but China is different because it still has an “industrial reserve army” of 700 million eager to flood into the cities. Ample low-wage labor will continue to fuel rapid growth, so China won't turn into tomorrow’s Japan.

Look again. China’s demography is a disaster. About 2015, the seemingly boundless labor pool will begin to shrink. One reason is rapid aging, which presages that China will become old before it becomes rich. By 2050, China will have lost one-third of its working-age population. Meanwhile, the U.S. will bestride the earth as the youngest industrialized nation after India.

Also in this decade, the number of China’s dependents will start to soar. The U.S. curve will rise only slowly, due to high fertility and immigration, two classic sources of rejuvenation. By midcentury, one Chinese worker will have to support two dependents, a ratio worse than anywhere in the West. If ample labor is the food of growth, China is looking at starvation.

Another data set should also have given pause to the World Bank: China’s cost advantage in manufacturing is almost history. Wages have risen exponentially since 2000, by an average of 19 percent annually. The figure for the U.S. was 4 percent.

As a study by Boston Consulting notes, “By around 2015, the total labor-cost savings of manufacturing many goods in China will be only 10 to 15 percent annually when actual labor content is factored in.” Subtract from this margin the cost of shipping and a global supply chain. So jobs are already wandering off to cheaper locales. Today it is Vietnam; tomorrow it will be Africa. Or the jobs will come home to the U.S., nourishing the country’s “re-industrialization” in tandem with plentiful cheap energy from fracking.

Finally, China’s politics are wrong. Authoritarian modernization -- call it “modernitarianism” -- runs up against its built-in limits, as did the Soviet Union’s. Frenzied industrialization under the knout of the party is easy, but the knowledge economy takes its cues from the markets. The watchword is “freedom” -- for entrepreneurs and capital, ideas and innovation. There is no Silicon Valley in China’s future.

Look at the assets that multiply returns. For instance, ask where human capital is being generated. U.S. education is always said to be in crisis. But 17 of the world’s top 20 universities are in the U.S., and 34 of the top 50. No other country produces more doctorates in science and engineering. Although 40 percent of the recipients come from abroad, two-thirds of them stay. Add triadic patents and citations in scientific journals, and it isn’t even a race between China and the U.S. This serendipitous story will continue, but it comes with a warning: The U.S. has to remain open and welcoming.

For now, don't waste time staring at the PPP snapshots, as kneaded and pummeled by the World Bank. They reflect the price of Big Macs, not III: innovation, ingenuity and invention. It will take a long time before China catches up -- if ever.

http://www.bloombergview.com/article...s-so-yesterday

“It is not a surprise that China’s economy is big but this is just because its population is big,” says Mr Mao. “China is big, but not strong.” (Mao Yushi)

gapapa sih klu modal ukuran PPP indonesia juga bisa bangga ngalahin korsel

Diubah oleh AkuCintaNanae 13-05-2014 18:57

0

2.7K

14

Komentar yang asik ya

Urutan

Terbaru

Terlama

Komentar yang asik ya

Komunitas Pilihan